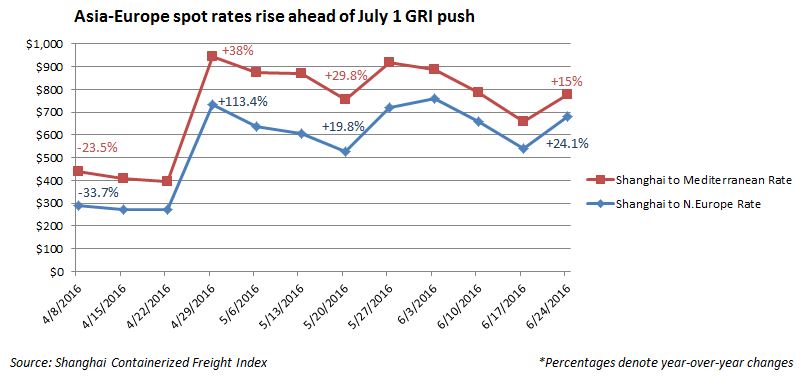

The latest reading of the Shanghai Containerized Freight Index shows the spot rate from Shanghai to North Europe rose $140 in the past week to $680 per 20-foot-equivalent unit, an increase of 26 percent. On Asia-Mediterranean routes the spot rate rose $116 to $776 per TEU, a weekly increase of 18 percent.

It was the opposite on the Asia-U.S. trades, where spot rates continued to decline for the third week running in the face of weak demand and the postponing of the July 1 GRI to July 15. Shanghai-U.S. West Coast rates slipped $17 to $753 per 40-foot-equivalent unit, while the all-water Asia-U.S. East Coast rate lost $32 to hit $1,496 per FEU, the SCFI reading showed. The weekly rates on all major trades are captured on JOC.com's Market Data Hub.

Rising rates on Asia-Europe will be welcome news for container lines as surplus capacity and weak demand had threatened to take the container price below the $500 per TEU threshold and further undermine next week’s GRIs, which will need all the help they can get.

Drewry said from January to mid-June, the GRI’s levied by carriers on Asia-Europe have totalled $4,900 per 40-foot container while the actual spot rate on June 16 was $1,077 per FEU. It hardly seems worth the effort as the rate increases are never fully successful and whatever increases are accepted by the market seldom stick longer than a week.

“Starting with 100 percent-plus price increases for one week, when carriers must know that the real effect after a few weeks will be much less, seems an abnormal see-saw way of pricing,” Drewry said in a logistics briefing note.

The low spot rates were placing shippers in an complicated position, said Xeneta Chief Executive Officer Patrik Berglund. He said based on historical data, short-term rates were always the first to go up or down, with long-term rates following their lead.

“This raises an interesting question for shippers — should they take advantage of long-term agreements now and lock in rates while they’re still low?” he said. “On the face of it, you’d say yes. But there are potentially serious risks involved. When container prices now begin to rise, those that have been booked in at a lower price may be shunted down the pecking order in favor of those that have agreed the new, higher rates. This phenomenon of short shipping is nothing new in the container market, with the carriers — who have been experiencing very difficult times — obviously keen to maximize the returns on each box.

“The danger of having cargo left at the quayside, and therefore losing sales and breaking the supply chain, is a worst nightmare scenario for a retailer, or any company that ships in large volumes,” Berglund said.

Trans-Pacific carriers are working to make rate increases stick by cutting capacity. China Cosco Shipping, the Ocean Three and the G6 Alliance have all cut services, resulting in a 1 percent drop in trans-Pacific capacity equal to 16,000 TEUs, according to Alphaliner.

This summer will usher in a new capacity environment with the opening at the end of this week of the third set of Panama Canal locks. Vessel sizes initially will probably double from about 4,500 TEUs today to ships of 8,000 TEUs to 10,000 TEUs. However, it will take some weeks for carriers to test the new locks and phase in their rotations.

Total U.S. import growth in 2016 is still very much in question, with the Global Port Tracker predicting minimal growth of about 1 percent from 2015. However, IHS Senior Economist Mario Moreno projects 5.7 percent growth.

{kind=link}